How Medical Practices Stay Independent and Profitable

July 30, 2025

Why Now Is the Time to Act on New Tariffs

August 1, 2025A Smart, Stress-Free Way to Offer Retirement Benefits

Understanding Safe Harbor 401(k) Plans

By Jessica Harrington

If you’re a small business owner looking to attract and keep top talent, offering a 401(k) plan is a powerful tool. But if you’ve ever dealt with the headaches of annual testing and compliance requirements that come with traditional plans, you know it’s not always easy, especially when most of your team’s compensation skews toward owners or high earners.

Enter the Safe Harbor 401(k): a simpler, smarter alternative designed to take the compliance burden off your plate.

Why Choose a Safe Harbor 401(k)?

With a Safe Harbor 401(k), your business agrees to make certain minimum contributions for employees. In exchange, you can skip most of the IRS’s nondiscrimination tests and give your highly compensated team members (including owners) the chance to max out their retirement savings without fear of triggering costly corrections later.

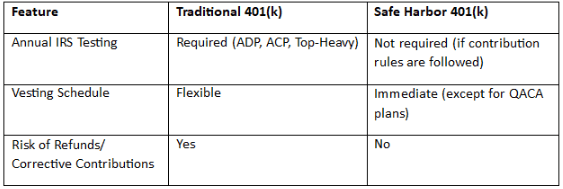

What Makes It Different from a Traditional 401(k)?

Let’s break down the key differences:

In a traditional plan, failing annual tests can mean issuing refunds to executives or making unexpected contributions for other employees. Safe Harbor plans help you avoid that altogether, as long as you stick to the contribution rules.

Your Safe Harbor Contribution Options

To qualify, you’ll need to commit to one of the following employer contribution formulas:

- Basic Match. Match 100% of the first 3% of pay an employee contributes, plus 50% of the next 2%.

- Enhanced Match. Typically, match 100% of contributions up to 4% (or more) of pay.

- Non-Elective Contribution. Contribute at least 3% of each employee’s pay, whether or not they participate.

- QACA (Qualified Automatic Contribution Arrangement): Start employees at a 3% automatic contribution, increasing to at least 6% over time. You’re allowed to use a lower match rate under this option.

Example: Say you have 10 employees, and the leadership team wants to contribute the maximum to their retirement accounts. A Safe Harbor plan ensures they can do that without worrying about failed testing or IRS penalties.

What About Vesting and Notifications?

In most cases, Safe Harbor contributions are 100% vested right away, meaning employees fully own that money as soon as it hits their account. The only exception is the QACA plan, which allows for a vesting period of up to two years.

You’ll also need to give your employees advance notice if you’re using a match-based or QACA plan, usually at least 30 days before the plan year starts. Thanks to the SECURE Act 2.0, if you choose the non-elective (≥3%) formula, you now only need to provide an initial notice and updates if anything changes.

Do I Still Need to Worry About Top-Heavy Rules?

Generally, no. Safe Harbor plans help you steer clear of most nondiscrimination and top-heavy issues, as long as you stick with the approved contribution formulas.

However, if you add other types of contributions (like profit sharing), your plan could still be considered top-heavy. That may trigger additional testing or required contributions, so it’s something to watch for.

401(k) Contribution Limits for 2025

Here’s what’s allowed for the upcoming plan year:

- Employee contributions: Up to $23,500

- Combined employee + employer contributions: Up to $70,000

- Catch-up contributions (age 50+): An extra $7,500

- Special catch-up (age 60–63): Up to $11,250 under SECURE Act 2.0

- Heads up: Starting in 2026, employees earning more than $145,000 must make catch-up contributions as Roth (after-tax)

What It Costs and What to Consider

Safe Harbor plans require a clear financial commitment. Once you send out your annual notice, you’re locked into that contribution for the year, with very limited options to change midstream.

That said, these contributions are tax-deductible for your business, and in return, you’re getting a plan that’s easier to manage. And you’ll have happier employees who can confidently save for retirement.

Setting Up or Updating a Safe Harbor 401(k)

New to Safe Harbor? You’ll need to set up your plan and notify employees at least 30 days before it takes effect, usually by October 1 if you want it to apply for the current year.

Already have a plan? You can add Safe Harbor provisions for the following year or even mid-year if you’re switching to the non-elective contribution formula (with a higher percentage). Timing matters, especially under the SECURE Act, so don’t wait too long.

Your best bet? Work with a qualified third-party administrator or plan provider who can handle the paperwork, deadlines, and communications, so nothing falls through the cracks.

What’s Right for You

A Safe Harbor 401(k) can be a game-changer for business owners who want to offer strong benefits without dealing with annual testing and compliance stress. It’s also a great way to reward your team and plan for your own financial future.

If you’re wondering whether a Safe Harbor plan makes sense for your company, our team can walk you through your options, run cost projections and help you align your plan with your broader business goals.